What families need to consider

According to the College Board, the most recently published figures of the average annual cost of tuition and fees at a public university for a school year was $9,970 for in-state students and $25,620 for out-of-state students. The average cost of a private university was much higher at $34,740.

Thankfully, much like tax-advantaged accounts designed to help us save for retirement, there are tax-advantaged accounts designed to help families set aside funds for future college costs. Named after Section 529 of the Internal Revenue Code and created in 1996, there are two types of tax-advantaged college savings programs: pre-paid tuition plans and college savings plans.

The attraction of 529 college savings programs is that both provide for investment earnings to grow on a tax-deferred basis. In addition, funds used to pay for qualified education expenses may be withdrawn free of tax. Nonqualified withdrawals, on the other hand, are subject to ordinary income tax and a 10% penalty on earnings. Let’s examine the differences.

Prepaid Tuition vs. College Savings Plans

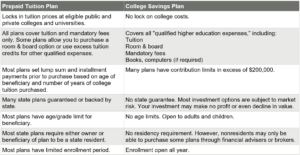

One type of 529 program is the prepaid tuition plan, which allows you to lock in tuition rates at eligible state colleges and universities.

Most are sponsored by state governments and allow account holders to “purchase” tuition at today’s rates and “redeem” the credits in the future when your child is going to college. In effect, the state is absorbing tuition increases during the years in between.

Pre-paid tuition plans allow you to pay for tuition in one payment today or through installments, but generally don’t cover expenses such as room and board. Your contributions are then pooled with other plan participants and invested by the state, then transferred to the appropriate school when your child starts college. But since the state is managing the investments, you have no investment options.

In contrast, college savings plan typically offer several investment options, at varying levels of risk, depending on how close the child is to college. Plus, college savings plans allow students to attend any accredited post-secondary school, public or private, irrespective of the state where you live or where the college is located.

In addition, although the investments are managed by a state-designated professional money manager – typically through mutual funds – and are allocated to mutual funds based on the age of your child (the beneficiary), you generally get to determine which investment is appropriate for you, based on your risk tolerance and other factors.

The investment objectives of the mutual funds are also what most people are familiar with: equity mutual funds, fixed-income mutual funds and money market mutual funds or age-based mutual funds that shift the allocation among stocks, bonds and cash depending on the age of your child. The following chart was copied from the Securities and Exchange Commission and outlines many of the major differences between prepaid tuition plans and college savings plans:

Which is Most Suitable for You?

Your own financial situation will determine whether

a prepaid tuition plan or college savings plan is the preferred vehicle to help someone through college. Part of this determination includes the effect that either will have on your student’s financial aid eligibility and your own estate planning. That being said, as a financial professional I worry about prepaid tuition plans for a few reasons:

First, there just are not that many states providing prepaid tuition plans and accepting new applications. Second, I really don’t like to rely on a state to fulfill

a financial guarantee, especially with shrinking

state budgets.

That doesn’t mean that college savings plans are not without flaws either. My “worry” with college savings plans are fewer, however: some college savings plans are very expensive and some don’t have great investment options from which to select. With a bit of homework, however, both of these worries can be mitigated.

The Key to Saving for College

The reality is that depending on the number of children you have, saving for college might be the most expensive item you encounter, outside of saving for your retirement. So much like I counsel clients with their retirement, the key is to start early so that your savings have more time to grow. Call me if you

have any questions or would like to start saving for

college today.

Important Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual security. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

This article was prepared by RSW Publishing.

LPL Tracking #1-05257820